DEKYAS NEWS World Breaking News and Trusted Source

DEKYAS NEWS World Breaking News and Trusted Source

Related Articles

Giselleflissak

Client discretionary shares have fallen off a cliff in latest months as traders weigh the affect of recession and inflation on earnings within the sector. Aggressive fee hikes by the Federal Reserve to battle inflation are anticipated to harm client discretionary spending into 2023.

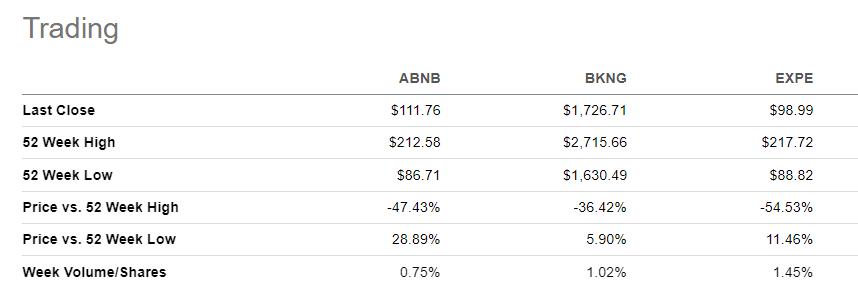

The journey and leisure business has been notably arduous hit, with on-line journey companies reminiscent of Airbnb, Inc. (NASDAQ:ABNB), Reserving Holdings Inc. (BKNG) and Expedia Group, Inc. (EXPE) all posting large declines of between 35% and 55% from their 52-week highs, because the chart under illustrates.

ABNB, BKNG and EXPE Buying and selling Historical past (In search of Alpha)

On-line journey companies make for a probably thrilling funding following these large declines. The sector is rising robustly, with all three highlighted names posting report earnings for most up-to-date quarters. The weak point in these shares is subsequently a terrific low cost from Mr. Market and an opportunity for bulls to revenue from the subsequent huge transfer up.

The most effective time to spend money on journey and leisure shares reminiscent of motels, airways, and on-line journey companies was in mid 2020 on the top of the Covid-induced panic previous to the vaccine popping out and previous to unemployment coming down from the mid-high teenagers ranges. The second greatest time is now, when the mainstream view is that the Fed’s continued fee hikes will crash the financial system and immediate a painful recession that may depart the journey and leisure sector with a nasty hangover. Whereas this view appears logical, the fears are undoubtedly overblown.

Repeatedly, the human want for journey and new experiences has confirmed to be resilient amid totally different sorts of headwinds. Although the financial system appears to be horrible, there’s an outdated saying that individuals don’t dwell to work, however work to dwell. And a giant a part of “dwelling” is touring, seeing new locations and folks, and having fun with new experiences. Shoppers can and doubtless will lower down on journey throughout arduous financial occasions, however they definitely will not remove it altogether. Actually, when financial fortunes inevitably change for the higher, customers are inclined to splurge like by no means earlier than, an idea business pundits name “revenge journey.”

On-line journey company shares are subsequently a really thrilling space to start out a place given the energy and resilience of the underlying enterprise and the bitter investor sentiment exemplified by large inventory declines. Tellingly, despite the fact that expectations for client spending began declining months in the past after the primary few fee hikes by the Fed, on-line journey companies have posted the very best working efficiency on report in accordance with the newest earnings stories. That is true for each ABNB and EXPE which posted report revenues within the quarters ended June 30. ABNB noticed quarterly revenues soar 57.6% yr over yr to $2.1 billion, whereas EXPE noticed an over 50% leap in income from the prior yr to $3.18 billion. BKNG guided for report revenues in Q3 after gross bookings rose 57% yr on yr to $34.5 billion in Q2.

Go along with ABNB

In our view, ABNB stands out as in comparison with BKNG and EXPE, regardless of being the “new child on the block” having solely gone public in December 2020. Each BKNG and EXPE went public in 1999 amid the dot com hype.

We expect ABNB has some clear aggressive benefits when it comes to its monetary form, enterprise mannequin, model energy, and skill to efficiently innovate at scale and tempo.

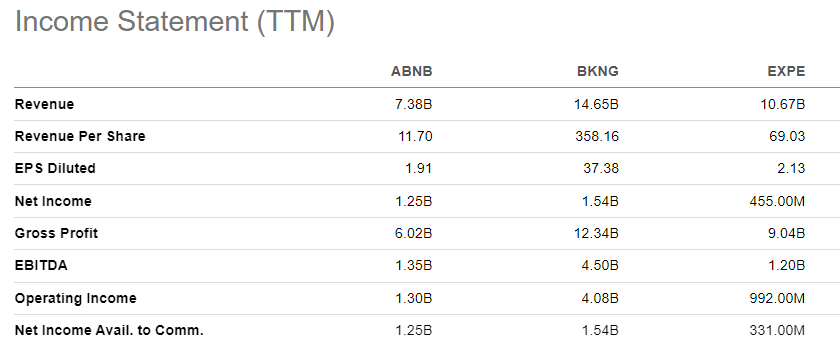

Let’s begin with the monetary form. ABNB has the least income for the trailing twelve months in contrast with BKNG and EXPE, because the chart under illustrates.

ABNB, BKNG and EXPE Revenue Assertion for ttm (In search of Alpha)

If you happen to zoom in and have a look at internet earnings, ABNB’s stronger monetary form relative to BKNG and EXPE is instantly obvious. Its $1.25 billion internet earnings for the trailing twelve months is greater than double EXPE’s and simply $250 million shy of BKNG’s, regardless of the latter two raking in between $Three and $7 billion extra in high line.

The explanation ABNB is making more cash for its shareholders for each greenback credited into its accounts by its clients is as a result of it has the very best working construction among the many three. EXPE has 14,800 workers and BKNG 19,450 workers, as per information on In search of Alpha. ABNB solely has 6,132. ABNB is leaner and, subsequently, extra worthwhile.

ABNB additionally has a robust model that reduces the necessity to “purchase” clients by aggressive advert spending and different pricey promotional exercise. It converts clients on the fraction of the associated fee EXPE and BKNG do, and it is a key energy that not solely offers it extra profitability, however extra monetary stability throughout business downturns, because the under instance reveals.

Commenting on how ABNB lower all its advertising and marketing to guard money and survive by the early phases of the pandemic, CEO Brian Chesky famous in a latest Goldman Sachs (GS) convention that:

“What occurs for those who flip off all of your advertising and marketing? You already know what occurred? Virtually nothing. Google didn’t need anybody to know this. However our site visitors got here again to greater than 90% of what it was after we turned off all of our advertising and marketing. And we realized a few issues. The very first thing we realized is that our model is extremely sturdy.”

ABNB has additionally confirmed that it will possibly innovate at tempo and scale. It has in latest months rolled out a number of attention-grabbing new merchandise.

The primary innovation price mentioning is the AirCover function for hosts and company. One of the simplest ways to know this function is as a type of insurance coverage that embeds belief and accountability inside the ABNB ecosystem. AirCover for hosts, which was first to launch, offers $1 million safety in opposition to property injury, $1 million private legal responsibility protection, so hosts not have to fret about strangers coming in and damaging their home. AirCover for company, which launched this summer season, principally offers a assure in opposition to the house not being as described, if you cannot get in or if the host cancels on you. CEO Brian Chesky famous within the Q2 earnings name that, since launch of AirCover for company, the Web Promoter Rating for company that had a problem with their keep has already improved. He additionally famous that in instances the place hosts cancel on a visitor, AirCover for Visitor has led to 10% extra rebookings.

ABNB additionally this summer season launched Airbnb Classes. The entire thought is to enhance the search performance past locations to incorporate distinctive experiences. Locations are limiting as the highest 100 cities will seemingly stay unchanged yr over yr. With experiences, reminiscent of tree homes, haunted mansions and different thrilling classes, ABNB is certain to get extra engagement and bookings as company get a higher number of choices to select from versus a generic search like “high Airbnbs in New York.” New hosts are additionally prone to be part of the platform as classes catch momentum, specializing in profitable niches. “Since launch, listings within the Airbnb Classes have been seen greater than 180 million occasions. By Classes, we’re distributing visitor discovery throughout extra locations and dates,” stated Brian on the earnings name.

ABNB’s administration appears assured of the long run. And no, we didn’t check with upbeat feedback in latest public communications by ABNB executives to reach at this conclusion. There’s one thing extra convincing than flowery phrases – capital allocation. The corporate’s administration lately introduced a $2 billion share repurchase program – an indicator that it believes its shares are nonetheless significantly discounted relative to the corporate’s long-term potential. It is price mentioning at this level that the corporate had whole debt of $2.38 billion in opposition to money of $9.9 billion in the latest quarter, making the purchase backs the very best use of its capital in our view.

The dangers to observe for

We’re shopping for ABNB, however are additionally aware of some dangers which we really feel our readers also needs to observe. The primary is the danger of underestimating the affect of the Fed’s fee hikes and fears of recession on investor psychology. The buyer discretionary sector strikes inversely with rates of interest. Although we’re of the view that journey and leisure is resilient, concern can result in over-selling of even the very best names reminiscent of ABNB. It is subsequently prudent for traders to handle their threat and be conscious of how they construct their positions, i.e., do not buy and make the most of dips to construct a very good common value. It appears apparent, however it by no means hurts restating.

ABNB additionally has a wealthy valuation. It’s buying and selling 51X P/E (fwd) compared to BKNG’s 23X and EXPE’s 31X. It’s buying and selling 23X EV/EBITDA (fwd) compared to BKNG’s 12X and EXPE’s 7.5X. The valuation might restrict the upside and enlarge the draw back. Nonetheless, once you consider ABNB’s enterprise high quality, a premium versus its friends appears justified. Furthermore, ABNB continues to be at an early stage of progress relative to its friends and this clearly comes with the next valuation as its full earnings potential continues to be removed from being realized.

The final threat price contemplating is regulatory threat. Some cities have legal guidelines that limit your capacity to host paying company for brief intervals. These legal guidelines are sometimes a part of a metropolis’s zoning or administrative codes. ABNB has had run-ins with a number of cities due to this, whereas different cities that do not have these legal guidelines have been mulling introducing them after strain from native motels.

Regardless of these dangers, we imagine ABNB is an efficient purchase. The weak point within the client discretionary sector has introduced down its share value to a stage we imagine doesn’t totally mirror the potential of the underlying enterprise.