DEKYAS NEWS World Breaking News and Trusted Source

DEKYAS NEWS World Breaking News and Trusted Source

Related Articles

The Cannabiz Company/iStock through Getty Photographs

A Fast Take On WM Know-how

WM Know-how, Inc. (NASDAQ:MAPS) reported its Q2 2022 monetary outcomes on August 9, 2022, lacking anticipated income and beating EPS estimates.

The corporate gives software program options to hashish retailers and types for his or her ecommerce and compliance wants.

Till the corporate sees materials income development from new markets corresponding to New York and New Jersey and reduces its working losses, I’m on Maintain for MAPS within the close to time period.

WM Know-how Overview

Irvine, California-based WM Know-how was based in 2008 to develop a platform and market (Weedmaps) for ecommerce capabilities associated to ordering hashish merchandise on-line.

The agency is headed by Chief Govt Officer Chris Beals, who joined the agency in 2015 and beforehand was Senior Vice President at Colbeck and Senior Company Counsel at Deutsche Telekom N.A.

The corporate’s main choices embrace:

Weedmaps on-line market

WM Enterprise Suite

Sprout CRM system

Cannveya supply and logistics

The agency acquires clients through its on-line efforts and thru its direct gross sales and advertising efforts to companies.

WM Know-how’s Market & Competitors

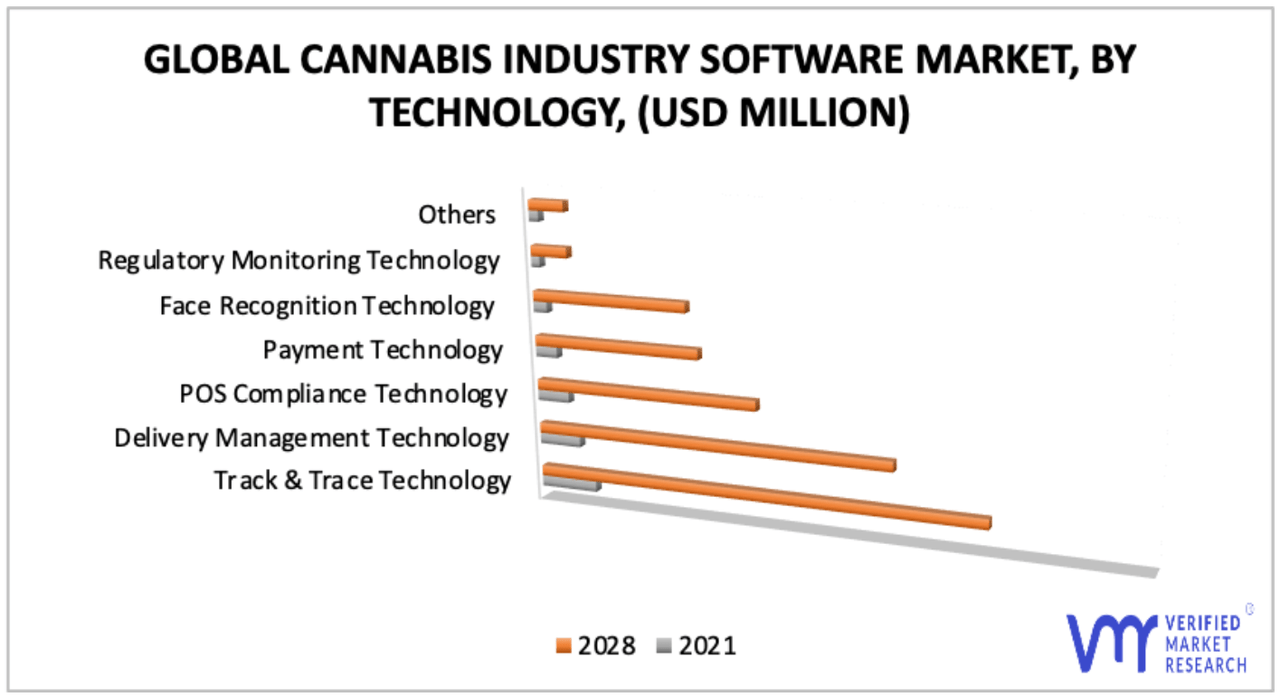

In accordance with a 2022 market analysis report by Verified Market Analysis, the worldwide marketplace for hashish trade software program was an estimated $$476 million in 2020 and is forecast to achieve $3.6 billion by 2028.

This represents a forecast CAGR of 30.18% from 2021 to 2028.

The primary drivers for this anticipated development are legalization successes leading to better regulation requiring elevated authorized compliance in addition to the necessity for efficiencies throughout hashish organizations.

Additionally, many international locations have legalized using hashish merchandise, a minimum of for therapeutic functions and in some circumstances leisure makes use of.

The chart beneath reveals the anticipated development trajectory of assorted hashish trade software program market applied sciences by way of 2028:

Hashish Trade Software program Market (Verified Market Analysis)

Main aggressive or different trade individuals embrace:

Ample Organics

Canix

Distru

Flourish Software program

Flowhub

Greenbits

Helix BioTrack

MJ Freeway

Retail Innovation Labs LLC (Cova Software program)

SYSPRO

WM Know-how’s Current Monetary Efficiency

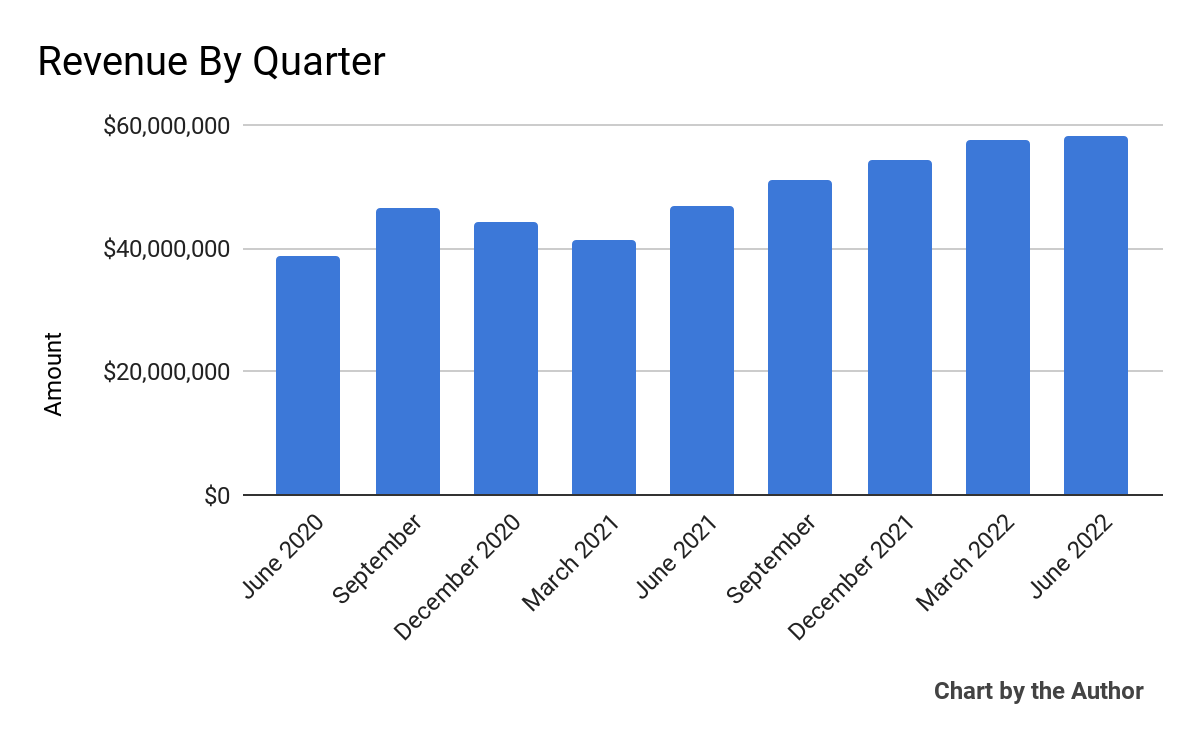

Whole income by quarter has risen in line with the next chart:

9 Quarter Whole Income (Looking for Alpha)

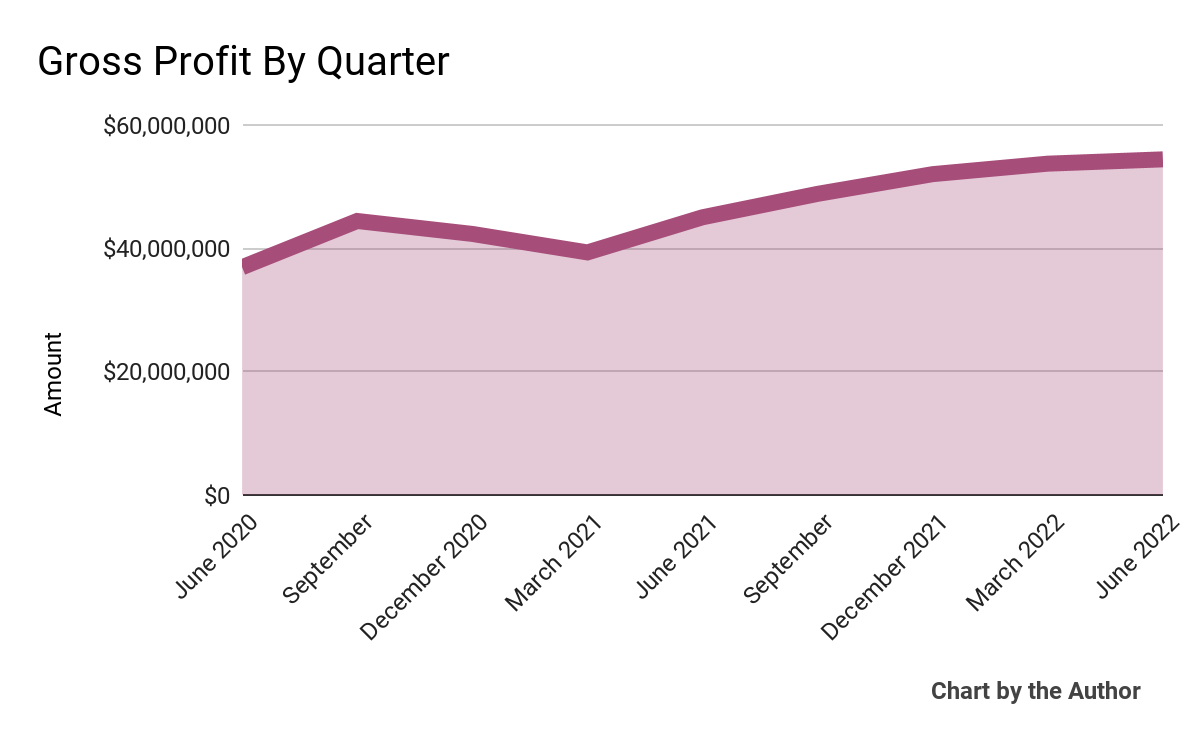

Gross revenue by quarter has adopted roughly the identical trajectory as whole income:

9 Quarter Gross Revenue (Looking for Alpha)

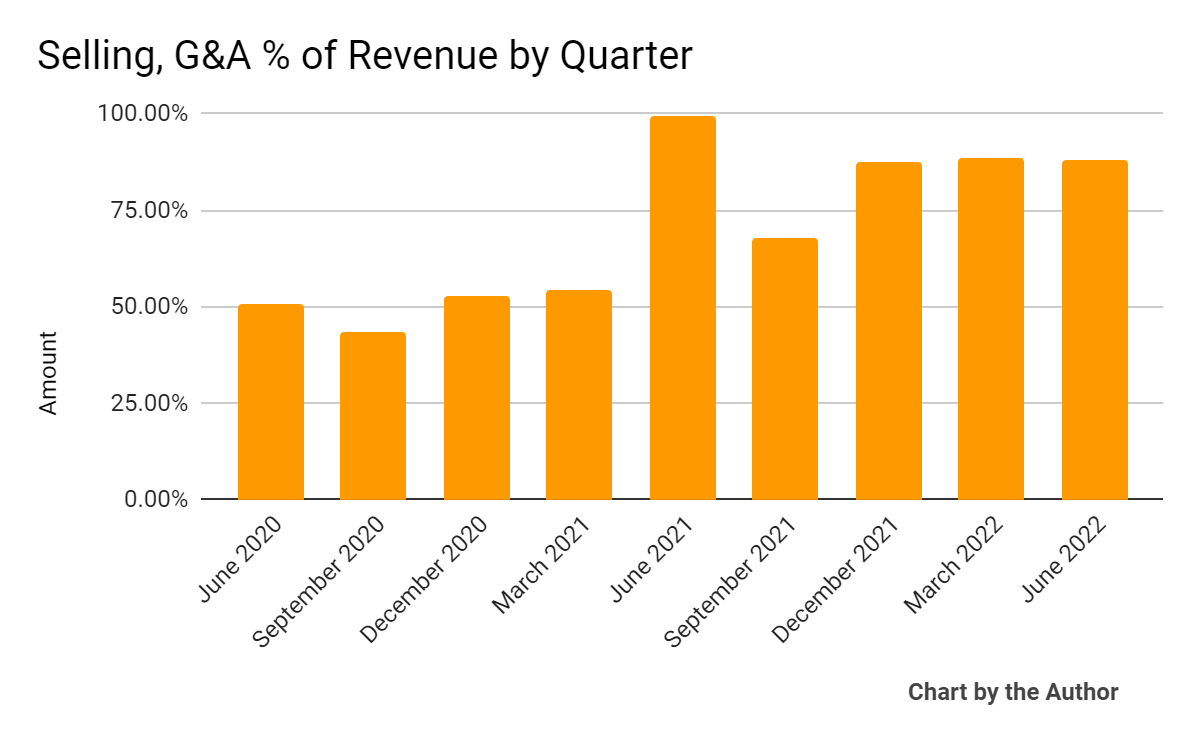

Promoting, G&A bills as a proportion of whole income by quarter have risen considerably in current quarters:

9 Quarter Promoting, G&A % Of Income (Looking for Alpha)

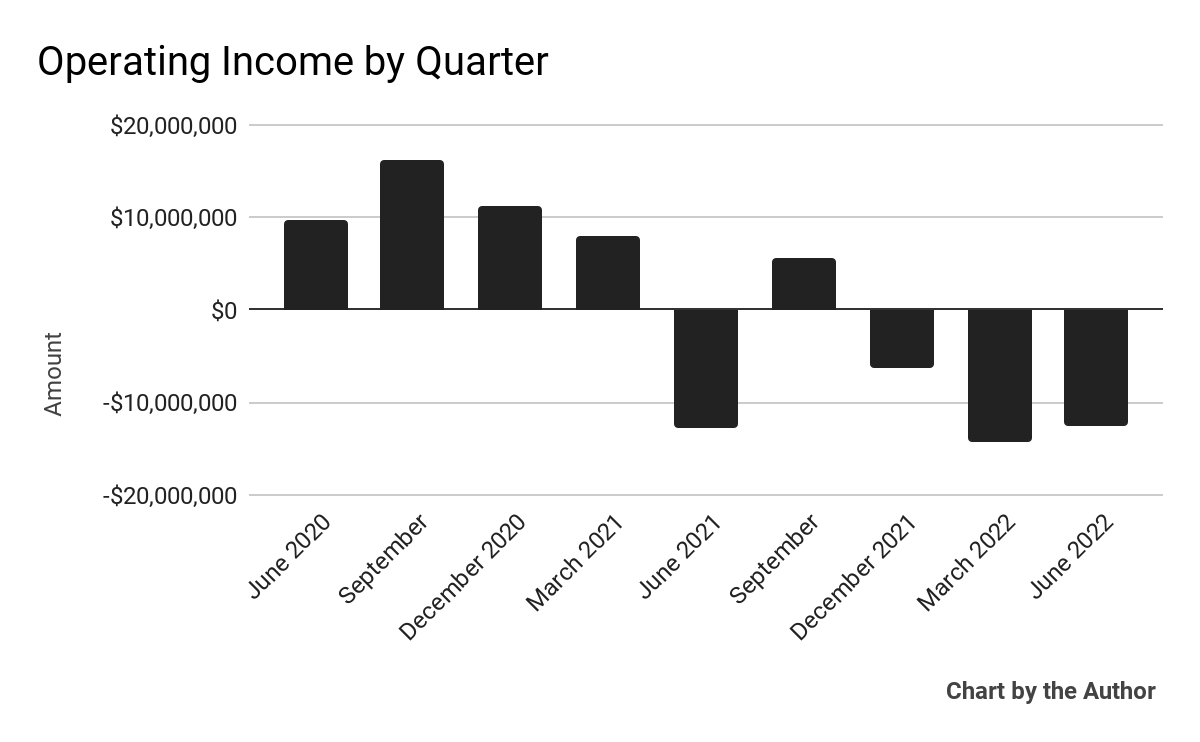

Working earnings by quarter has turned adverse in current quarters:

9 Quarter Working Revenue (Looking for Alpha)

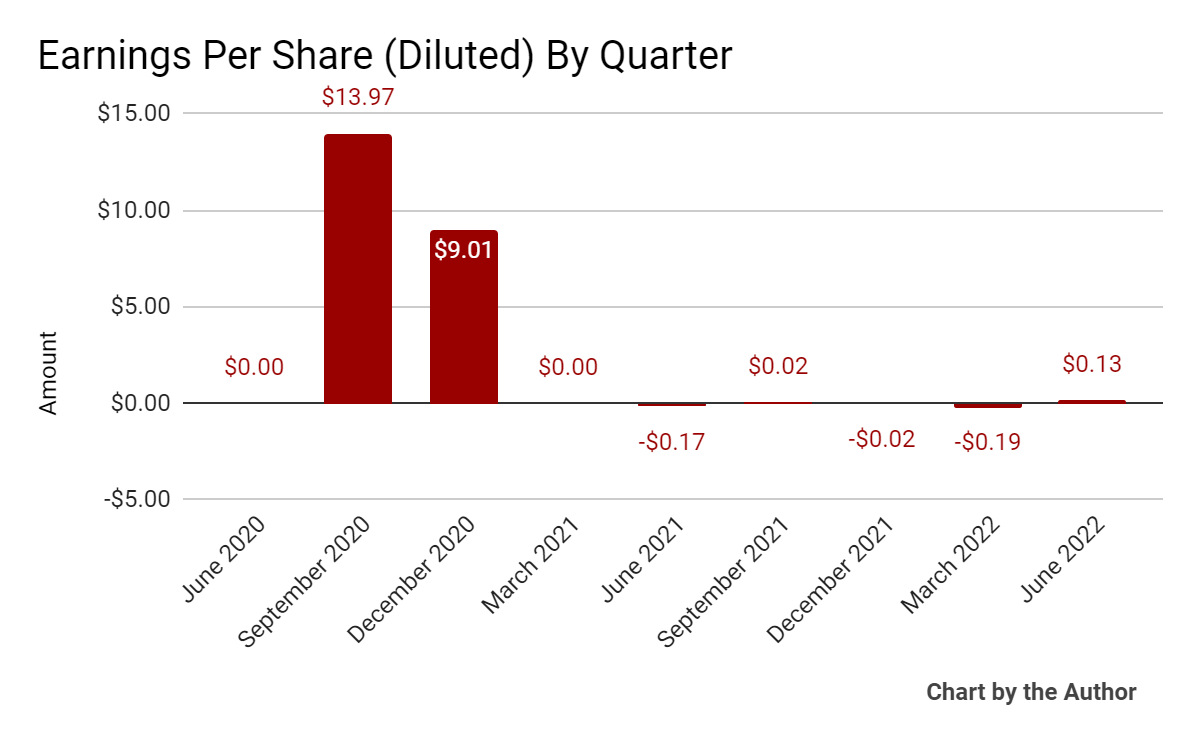

Earnings per share (Diluted) have fluctuated in line with the chart beneath:

9 Quarter Earnings Per Share (Looking for Alpha)

(All information in above charts is GAAP.)

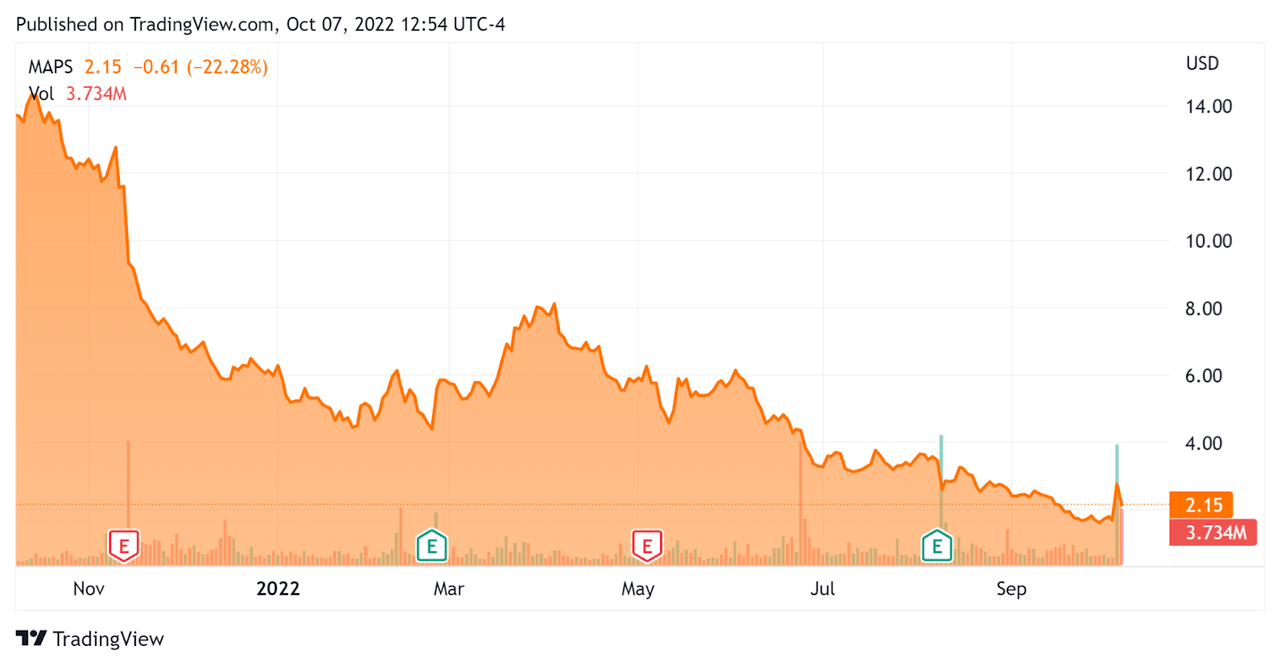

Prior to now 12 months, MAPS’ inventory value has fallen 84.6% vs. the U.S. S&P 500 index’s drop of round 16.5%, because the chart beneath signifies:

52 Week Inventory Value (Looking for Alpha)

Valuation And Different Metrics For WM Know-how

Beneath is a desk of related capitalization and valuation figures for the corporate:

Measure [TTM] | Quantity |

Enterprise Worth / Gross sales | 0.92 |

Income Progress Price | 23.4% |

Web Revenue Margin | 24.4% |

GAAP EBITDA % | -8.9% |

Market Capitalization | $270,550,000 |

Enterprise Worth | $203,780,000 |

Working Money Circulation | $2,740,000 |

Earnings Per Share (Totally Diluted) | -$0.06 |

(Supply – Looking for Alpha)

The Rule of 40 is a software program trade rule of thumb that claims that so long as the mixed income development charge and EBITDA proportion charge equal or exceed 40%, the agency is on an appropriate development/EBITDA trajectory.

MAPS’ most up-to-date GAAP Rule of 40 calculation was 14.5% as of Q2 2022, so the agency wants vital enchancment on this regard, per the desk beneath:

Rule of 40 – GAAP | Calculation |

Current Rev. Progress % | 23.4% |

GAAP EBITDA % | -8.9% |

Whole | 14.5% |

(Supply – Looking for Alpha)

Commentary On WM Know-how

In its final earnings name (Supply – Looking for Alpha), masking Q2 2022’s outcomes, administration highlighted that its shortfall in outcomes was resulting from “macro challenges, specifically the numerous rise in fuel costs and different inflationary pressures in the course of the quarter.”

The agency has been compelled to take away sure purchasers from its platform resulting from non-payment and expects inflation and different financial pressures to extend on its purchasers in the course of the second half of 2022.

That is regardless of elevated optimism about extra states “trying poised to cross new legalization measures within the subsequent two years.”

Additionally of observe is the current motion by the President to pardon these discovered responsible on the federal stage of straightforward marijuana possession, or roughly 6,500 individuals.

As to its monetary outcomes, income rose 24% year-over-year regardless of vital declines in licensed channels throughout its markets.

The corporate’s web greenback retention charge for the month of June was 92%, indicating worsening outcomes resulting from practically 500 purchasers unable to pay or being placed on fee plans.

WM’s Rule of 40 outcomes have been sub-par, though the corporate isn’t strictly a software program agency.

Gross margin of 93% was flat sequentially whereas SG&A as a % of income remained elevated.

Consequently, working losses remained nicely above $10 million for the second quarter in a row.

For the stability sheet, the corporate ended the quarter with $47.6 million in money and no long-term debt.

Over the trailing twelve months, free money used was $13.Zero million because the agency made $15.7 million in capital expenditures.

Wanting forward, administration expects Q3 income development to be within the “low double-digit” vary and isn’t assuming any materials income contribution from both New Jersey or New York within the present fiscal yr.

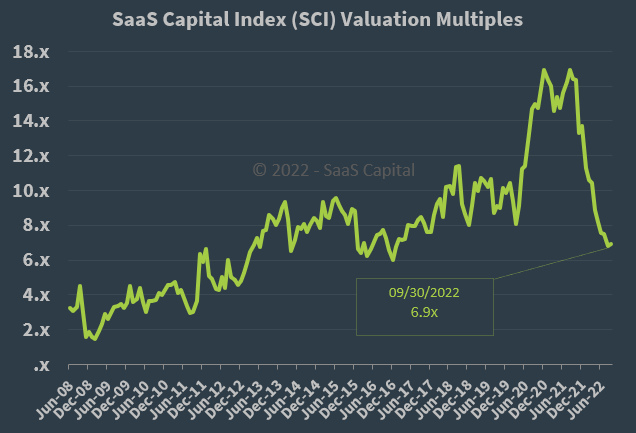

Concerning valuation, the market is valuing MAPS at an EV/Gross sales a number of of round 0.92x.

The SaaS Capital Index of publicly held SaaS (software program as a service) software program firms confirmed a median ahead EV/Income a number of of round 6.9x at September 30, 2022, because the chart reveals right here:

SaaS Capital Index (SaaS Capital)

So, by comparability, MAPS is at present valued by the market at a big low cost to the broader SaaS Capital Index, a minimum of as of September 30, 2022.

The first danger to the corporate’s outlook is a macroeconomic slowdown or recession, decreased entry to capital for potential licensees, each of which can gradual gross sales cycles and cut back its income development trajectory.

With the current employment figures indicating additional power within the U.S. economic system, it’s more and more seemingly the usFederal Reserve will proceed to extend rates of interest, growing the price of capital and lowering its availability within the course of.

This can seemingly exert additional downward stress on the corporate’s potential clients whereas lowering MAPS’ valuation a number of given its working loss place.

Till the corporate sees materials income development from new markets corresponding to New York and New Jersey and reduces its working losses, I’m on Maintain for MAPS within the close to time period.