DEKYAS NEWS World Breaking News and Trusted Source

DEKYAS NEWS World Breaking News and Trusted Source

Related Articles

Discovering a enterprise that has the potential to develop considerably isn’t simple, however it’s potential if we take a look at a number of key monetary metrics. Amongst different issues, we’ll need to see two issues; firstly, a rising return on capital employed (ROCE) and secondly, an enlargement within the firm’s quantity of capital employed. Mainly which means an organization has worthwhile initiatives that it might proceed to reinvest in, which is a trait of a compounding machine. So on that word, Amkor Expertise (NASDAQ:AMKR) seems fairly promising with reference to its developments of return on capital.

Understanding Return On Capital Employed (ROCE)

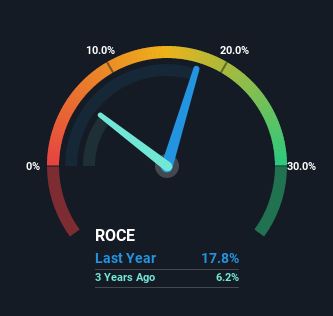

If you have not labored with ROCE earlier than, it measures the ‘return’ (pre-tax revenue) an organization generates from capital employed in its enterprise. To calculate this metric for Amkor Expertise, that is the components:

Return on Capital Employed = Earnings Earlier than Curiosity and Tax (EBIT) ÷ (Whole Belongings – Present Liabilities)

0.18 = US$820m ÷ (US$6.4b – US$1.8b) (Primarily based on the trailing twelve months to June 2022).

Thus, Amkor Expertise has an ROCE of 18%. In absolute phrases, that is a fairly regular return, and it is considerably near the Semiconductor business common of 15%.

Within the above chart now we have measured Amkor Expertise’s prior ROCE in opposition to its prior efficiency, however the future is arguably extra necessary. Should you’re , you may view the analysts predictions in our free report on analyst forecasts for the corporate.

So How Is Amkor Expertise’s ROCE Trending?

Amkor Expertise is displaying some optimistic developments. The information exhibits that returns on capital have elevated considerably over the past 5 years to 18%. Mainly the enterprise is incomes extra per greenback of capital invested and along with that, 54% extra capital is being employed now too. This may point out that there is loads of alternatives to take a position capital internally and at ever greater charges, a mix that is frequent amongst multi-baggers.

In Conclusion…

An organization that’s rising its returns on capital and might constantly reinvest in itself is a extremely wanted trait, and that is what Amkor Expertise has. For the reason that inventory has returned a stable 77% to shareholders over the past 5 years, it is honest to say buyers are starting to acknowledge these modifications. In mild of that, we predict it is price trying additional into this inventory as a result of if Amkor Expertise can maintain these developments up, it might have a vibrant future forward.

Whereas Amkor Expertise seems spectacular, no firm is price an infinite value. The intrinsic worth infographic in our free analysis report helps visualize whether or not AMKR is at present buying and selling for a good value.

Whereas Amkor Expertise could not at present earn the very best returns, we have compiled a listing of corporations that at present earn greater than 25% return on fairness. Try this free record right here.

Have suggestions on this text? Involved concerning the content material? Get in contact with us straight. Alternatively, electronic mail editorial-team (at) simplywallst.com.

This text by Merely Wall St is common in nature. We offer commentary based mostly on historic knowledge and analyst forecasts solely utilizing an unbiased methodology and our articles will not be meant to be monetary recommendation. It doesn’t represent a suggestion to purchase or promote any inventory, and doesn’t take account of your targets, or your monetary state of affairs. We purpose to carry you long-term centered evaluation pushed by basic knowledge. Notice that our evaluation could not issue within the newest price-sensitive firm bulletins or qualitative materials. Merely Wall St has no place in any shares talked about.

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially mirror these of Nasdaq, Inc.